Credit for image above: Twitter – @VoteSawant

NOTE: No mention of the centrality of racism and sexism the plays in “rigged” capitalism. I put rigged in quotes because it’s redundant to call capitalism rigged! Capitalism has always been rigged against the vast majority of the people: those exterminated or enslaved by capitalism’s founders and those who eventually became the proletariat all over the world. Hence, this essay is fundamentally flawed in its attempt to explain why their is a growing disparity between the haves and the have-nots. The accumulation of capitalist wealth is grounded upon stolen land, stolen people, sexism and genocide. Stiglitz here and French economist Thomas Piketty both offer good, but incomplete, economic analysis of capitalism today. To get a more accurate analysis of 21st century Capitalism, folks should read:

- What Did Cedric Robinson Mean by Racial Capitalism? by Robin D. G. Kelley

- Global Capitalism: Crisis of Humanity and the Specter of 21st Century Fascism

- Global Capitalism: What’s Race Got to Do with It?

- Race and Capitalism

- Global Capitalism, Immigrant Labour, and the Struggle for Justice

The American Economy Is Rigged

And what we can do about it.

By Joseph E. Stiglitz, Scientific American —

Americans are used to thinking that their nation is special. In many ways, it is: the U.S. has by far the most Nobel Prize winners, the largest defense expenditures (almost equal to the next 10 or so countries put together) and the most billionaires (twice as many as China, the closest competitor). But some examples of American Exceptionalism should not make us proud. By most accounts, the U.S. has the highest level of economic inequality among developed countries. It has the world’s greatest per capita health expenditures yet the lowest life expectancy among comparable countries. It is also one of a few developed countries jostling for the dubious distinction of having the lowest measures of equality of opportunity.

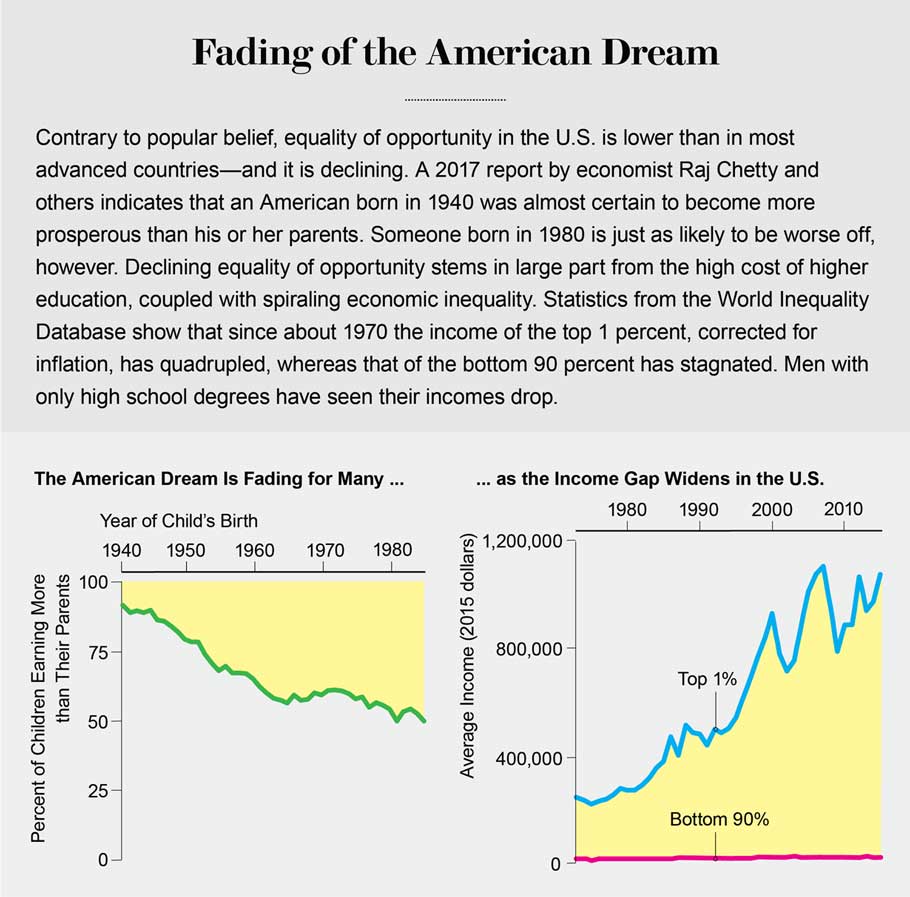

The notion of the American Dream—that, unlike old Europe, we are a land of opportunity—is part of our essence. Yet the numbers say otherwise. The life prospects of a young American depend more on the income and education of his or her parents than in almost any other advanced country. When poor-boy-makes-good anecdotes get passed around in the media, that is precisely because such stories are so rare.

Things appear to be getting worse, partly as a result of forces, such as technology and globalization, that seem beyond our control, but most disturbingly because of those within our command. It is not the laws of nature that have led to this dire situation: it is the laws of humankind. Markets do not exist in a vacuum: they are shaped by rules and regulations, which can be designed to favor one group over another. President Donald Trump was right in saying that the system is rigged—by those in the inherited plutocracy of which he himself is a member. And he is making it much, much worse.

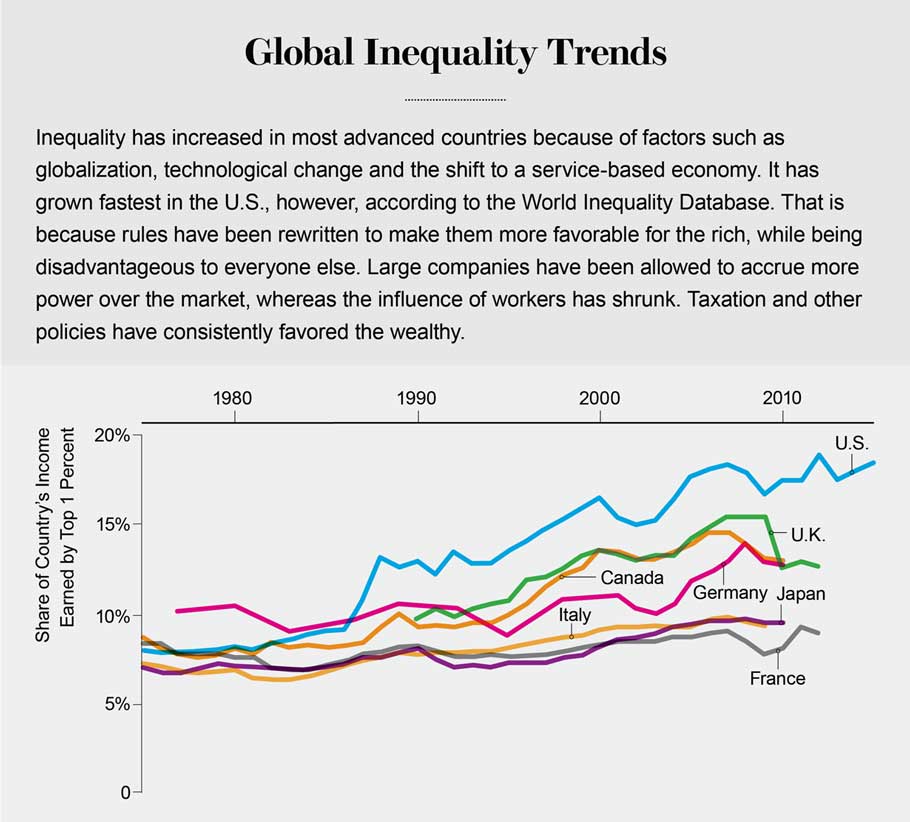

America has long outdone others in its level of inequality, but in the past 40 years it has reached new heights. Whereas the income share of the top 0.1 percent has more than quadrupled and that of the top 1 percent has almost doubled, that of the bottom 90 percent has declined. Wages at the bottom, adjusted for inflation, are about the same as they were some 60 years ago! In fact, for those with a high school education or less, incomes have fallen over recent decades. Males have been particularly hard hit, as the U.S. has moved away from manufacturing industries into an economy based on services.

DEATHS OF DESPAIR

Wealth is even less equally distributed, with just three Americans having as much as the bottom 50 percent—testimony to how much money there is at the top and how little there is at the bottom. Families in the bottom 50 percent hardly have the cash reserves to meet an emergency. Newspapers are replete with stories of those for whom the breakdown of a car or an illness starts a downward spiral from which they never recover.

In significant part because of high inequality [see “The Health-Wealth Gap,” by Robert M. Sapolsky], U.S. life expectancy, exceptionally low to begin with, is experiencing sustained declines. This in spite of the marvels of medical science, many advances of which occur right here in America and which are made readily available to the rich. Economist Ann Case and 2015 Nobel laureate in economics Angus Deaton describe one of the main causes of rising morbidity—the increase in alcoholism, drug overdoses and suicides—as “deaths of despair” by those who have given up hope.

Credit: Jen Christiansen; Sources: “The Fading American Dream: Trends in Absolute Income Mobility Since 1940,” by Raj Chetty et al., in Science, Vol. 356; April 28, 2017 (child-parent wealth comparison); World Inequality database (90% versus 1% wealth trend data)

Defenders of America’s inequality have a pat explanation. They refer to the workings of a competitive market, where the laws of supply and demand determine wages, prices and even interest rates—a mechanical system, much like that describing the physical universe. Those with scarce assets or skills are amply rewarded, they argue, because of the larger contributions they make to the economy. What they get merely represents what they have contributed. Often they take out less than they contributed, so what is left over for the rest is that much more.

This fictional narrative may at one time have assuaged the guilt of those at the top and persuaded everyone else to accept this sorry state of affairs. Perhaps the defining moment exposing the lie was the 2008 financial crisis, when the bankers who brought the global economy to the brink of ruin with predatory lending, market manipulation and various other antisocial practices walked away with millions of dollars in bonuses just as millions of Americans lost their jobs and homes and tens of millions more worldwide suffered on their account. Virtually none of these bankers were ever held to account for their misdeeds.

I became aware of the fantastical nature of this narrative as a schoolboy, when I thought of the wealth of the plantation owners, built on the backs of slaves. At the time of the Civil War, the market value of the slaves in the South was approximately half of the region’s total wealth, including the value of the land and the physical capital—the factories and equipment. The wealth of at least this part of this nation was not based on industry, innovation and commerce but rather on exploitation. Today we have replaced this open exploitation with more insidious forms, which have intensified since the Reagan-Thatcher revolution of the 1980s. This exploitation, I will argue, is largely to blame for the escalating inequality in the U.S.

After the New Deal of the 1930s, American inequality went into decline. By the 1950s inequality had receded to such an extent that another Nobel laureate in economics, Simon Kuznets, formulated what came to be called Kuznets’s law. In the early stages of development, as some parts of a country seize new opportunities, inequalities grow, he postulated; in the later stages, they shrink. The theory long fit the data—but then, around the early 1980s, the trend abruptly reversed.

EXPLAINING INEQUALITY

Image Credit: inequality.org

Economists have put forward a range of explanations for why inequality has in fact been increasing in many developed countries. Some argue that advances in technology have spurred the demand for skilled labor relative to unskilled labor, thereby depressing the wages of the latter. Yet that alone cannot explain why even skilled labor has done so poorly over the past two decades, why average wages have done so badly and why matters are so much worse in the U.S. than in other developed nations. Changes in technology are global and should affect all advanced economies in the same way. Other economists blame globalization itself, which has weakened the power of workers. Firms can and do move abroad unless demands for higher wages are curtailed. But again, globalization has been integral to all advanced economies. Why is its impact so much worse in the U.S.?

The shift from a manufacturing to a service-based economy is partly to blame. At its extreme—a firm of one person—the service economy is a winner-takes-all system. A movie star makes millions, for example, whereas most actors make a pittance. Overall, wages are likely to be far more widely dispersed in a service economy than in one based on manufacturing, so the transition contributes to greater inequality. This fact does not explain, however, why the average wage has not improved for decades. Moreover, the shift to the service sector is happening in most other advanced countries: Why are matters so much worse in the U.S.?

Again, because services are often provided locally, firms have more market power: the ability to raise prices above what would prevail in a competitive market. A small town in rural America may have only one authorized Toyota repair shop, which virtually every Toyota owner is forced to patronize. The providers of these local services can raise prices over costs, increasing their profits and the share of income going to owners and managers. This, too, increases inequality. But again, why is U.S. inequality practically unique?

In his celebrated 2013 treatise Capital in the Twenty-First Century, French economist Thomas Piketty shifts the gaze to capitalists. He suggests that the few who own much of a country’s capital save so much that, given the stable and high return to capital (relative to the growth rate of the economy), their share of the national income has been increasing. His theory has, however, been questioned on many grounds. For instance, the savings rate of even the rich in the U.S. is so low, compared with the rich in other countries, that the increase in inequality should be lower here, not greater.

An alternative theory is far more consonant with the facts. Since the mid-1970s the rules of the economic game have been rewritten, both globally and nationally, in ways that advantage the rich and disadvantage the rest. And they have been rewritten further in this perverse direction in the U.S. than in other developed countries—even though the rules in the U.S. were already less favorable to workers. From this perspective, increasing inequality is a matter of choice: a consequence of our policies, laws and regulations.

In the U.S., the market power of large corporations, which was greater than in most other advanced countries to begin with, has increased even more than elsewhere. On the other hand, the market power of workers, which started out less than in most other advanced countries, has fallen further than elsewhere. This is not only because of the shift to a service-sector economy—it is because of the rigged rules of the game, rules set in a political system that is itself rigged through gerrymandering, voter suppression and the influence of money. A vicious spiral has formed: economic inequality translates into political inequality, which leads to rules that favor the wealthy, which in turn reinforces economic inequality.

FEEDBACK LOOP

Political scientists have documented the ways in which money influences politics in certain political systems, converting higher economic inequality into greater political inequality. Political inequality, in its turn, gives rise to more economic inequality as the rich use their political power to shape the rules of the game in ways that favor them—for instance, by softening antitrust laws and weakening unions. Using mathematical models, economists such as myself have shown that this two-way feedback loop between money and regulations leads to at least two stable points. If an economy starts out with lower inequality, the political system generates rules that sustain it, leading to one equilibrium situation. The American system is the other equilibrium—and will continue to be unless there is a democratic political awakening.

An account of how the rules have been shaped must begin with antitrust laws, first enacted 128 years ago in the U.S. to prevent the agglomeration of market power. Their enforcement has weakened—at a time when, if anything, the laws themselves should have been strengthened. Technological changes have concentrated market power in the hands of a few global players, in part because of so-called network effects: you are far more likely to join a particular social network or use a certain word processor if everyone you know is already using it. Once established, a firm such as Facebook or Microsoft is hard to dislodge. Moreover, fixed costs, such as that of developing a piece of software, have increased as compared with marginal costs—that of duplicating the software. A new entrant has to bear all these fixed costs up front, and if it does enter, the rich incumbent can respond by lowering prices drastically. The cost of making an additional e-book or photo-editing program is essentially zero.

In short, entry is hard and risky, which gives established firms with deep war chests enormous power to crush competitors and ultimately raise prices. Making matters worse, U.S. firms have been innovative not only in the products they make but in thinking of ways to extend and amplify their market power. The European Commission has imposed fines of billions of dollars on Microsoft and Google and ordered them to stop their anticompetitive practices (such as Google privileging its own comparison shopping service). In the U.S., we have done too little to control concentrations of market power, so it is not a surprise that it has increased in many sectors.

Credit: Jen Christiansen; Sources: Economic Report of the President. January 2017; World Inequality database

Rigged rules also explain why the impact of globalization may have been worse in the U.S. A concerted attack on unions has almost halved the fraction of unionized workers in the nation, to about 11 percent. (In Scandinavia, it is roughly 70 percent.) Weaker unions provide workers less protection against the efforts of firms to drive down wages or worsen working conditions. Moreover, U.S. investment treaties such as the North Atlantic Free Trade Agreement—treaties that were sold as a way of preventing foreign countries from discriminating against American firms—also protect investors against a tightening of environmental and health regulations abroad. For instance, they enable corporations to sue nations in private international arbitration panels for passing laws that protect citizens and the environment but threaten the multinational company’s bottom line. Firms like these provisions, which enhance the credibility of a company’s threat to move abroad if workers do not temper their demands. In short, these investment agreements weaken U.S. workers’ bargaining power even further.

LIBERATED FINANCE

Many other changes to our norms, laws, rules and regulations have contributed to inequality. Weak corporate governance laws have allowed chief executives in the U.S. to compensate themselves 361 times more than the average worker, far more than in other developed countries. Financial liberalization—the stripping away of regulations designed to prevent the financial sector from imposing harms, such as the 2008 economic crisis, on the rest of society—has enabled the finance industry to grow in size and profitability and has increased its opportunities to exploit everyone else. Banks routinely indulge in practices that are legal but should not be, such as imposing usurious interest rates on borrowers or exorbitant fees on merchants for credit and debit cards and creating securities that are designed to fail. They also frequently do things that are illegal, including market manipulation and insider trading. In all of this, the financial sector has moved money away from ordinary Americans to rich bankers and the banks’ shareholders. This redistribution of wealth is an important contributor to American inequality.

Other means of so-called rent extraction—the withdrawal of income from the national pie that is incommensurate with societal contribution—abound. For example, a legal provision enacted in 2003 prohibited the government from negotiating drug prices for Medicare—a gift of some $50 billion a year or more to the pharmaceutical industry. Special favors, such as extractive industries’ obtaining public resources such as oil at below fair-market value or banks’ getting funds from the Federal Reserve at near-zero interest rates (which they relend at high interest rates), also amount to rent extraction. Further exacerbating inequality is favorable tax treatment for the rich. In the U.S., those at the top pay a smaller fraction of their income in taxes than those who are much poorer—a form of largesse that the Trump administration has just worsened with the 2017 tax bill.

Some economists have argued that we can lessen inequality only by giving up on growth and efficiency. But recent research, such as work done by Jonathan Ostry and others at the International Monetary Fund, suggests that economies with greater equality perform better, with higher growth, better average standards of living and greater stability. Inequality in the extremes observed in the U.S. and in the manner generated there actually damages the economy. The exploitation of market power and the variety of other distortions I have described, for instance, makes markets less efficient, leading to underproduction of valuable goods such as basic research and overproduction of others, such as exploitative financial products.

Credit: Jen Christiansen; Sources: World Inequality Report 2018. World Inequality Lab, 2017; Branko Milanovic

Moreover, because the rich typically spend a smaller fraction of their income on consumption than the poor, total or “aggregate” demand in countries with higher inequality is weaker. Societies could make up for this gap by increasing government spending—on infrastructure, education and health, for instance, all of which are investments necessary for long-term growth. But the politics of unequal societies typically puts the burden on monetary policy: interest rates are lowered to stimulate spending. Artificially low interest rates, especially if coupled with inadequate financial market regulation, often give rise to bubbles, which is what happened with the 2008 housing crisis.

It is no surprise that, on average, people living in unequal societies have less equality of opportunity: those at the bottom never get the education that would enable them to live up to their potential. This fact, in turn, exacerbates inequality while wasting the country’s most valuable resource: Americans themselves.

RESTORING JUSTICE

Morale is lower in unequal societies, especially when inequality is seen as unjust, and the feeling of being used or cheated leads to lower productivity. When those who run gambling casinos or bankers suffering from moral turpitude make a zillion times more than the scientists and inventors who brought us lasers, transistors and an understanding of DNA, it is clear that something is wrong. Then again, the children of the rich come to think of themselves as a class apart, entitled to their good fortune, and accordingly more likely to break the rules necessary for making society function. All of this contributes to a breakdown of trust, with its attendant impact on social cohesion and economic performance.

There is no magic bullet to remedy a problem as deep-rooted as America’s inequality. Its origins are largely political, so it is hard to imagine meaningful change without a concerted effort to take money out of politics—through, for instance, campaign finance reform. Blocking the revolving doors by which regulators and other government officials come from and return to the same industries they regulate and work with is also essential.

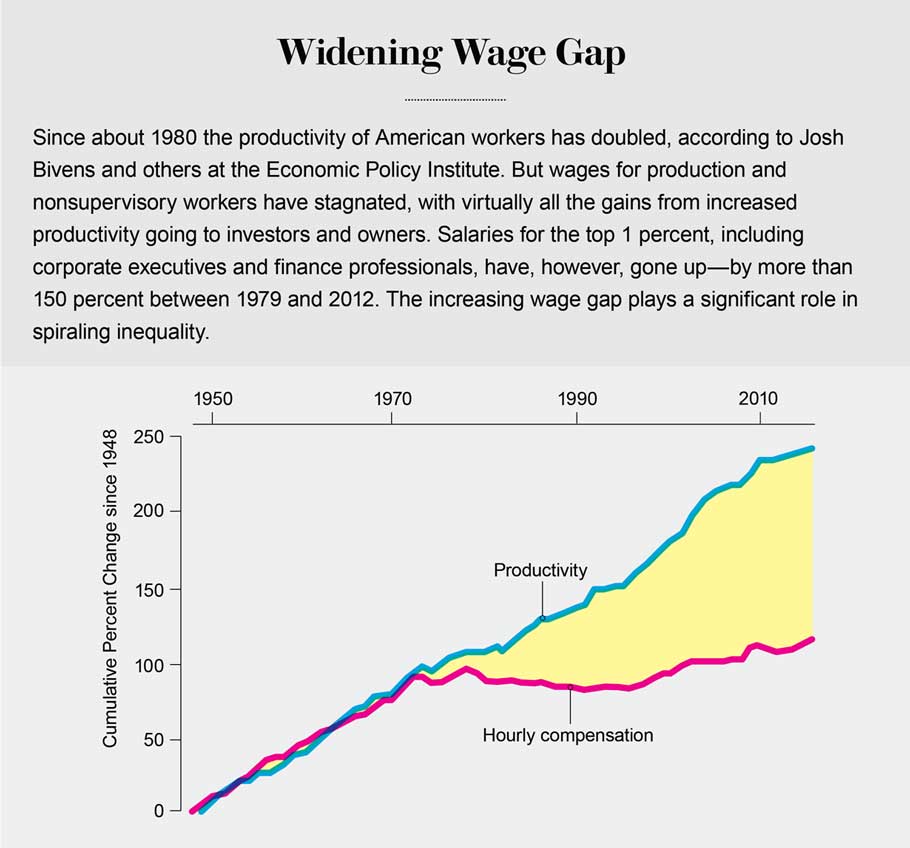

Credit: Jen Christiansen; Sources: Raising America’s Pay: Why It’s Our Central Economic Policy Challenge, by Josh Bivens et al. Economic Policy Institute, June 4, 2014; The State of Working America, by Lawrence Mishel, Josh Bivens, Elise Gould and Heidi Shierholz. 12th Edition. ILR Press, 2012

Beyond that, we need more progressive taxation and high-quality federally funded public education, including affordable access to universities for all, no ruinous loans required. We need modern competition laws to deal with the problems posed by 21st-century market power and stronger enforcement of the laws we do have. We need labor laws that protect workers and their rights to unionize. We need corporate governance laws that curb exorbitant salaries bestowed on chief executives, and we need stronger financial regulations that will prevent banks from engaging in the exploitative practices that have become their hallmark. We need better enforcement of antidiscrimination laws: it is unconscionable that women and minorities get paid a mere fraction of what their white male counterparts receive. We also need more sensible inheritance laws that will reduce the intergenerational transmission of advantage and disadvantage.

The basic perquisites of a middle-class life, including a secure old age, are no longer attainable for most Americans. We need to guarantee access to health care. We need to strengthen and reform retirement programs, which have put an increasing burden of risk management on workers (who are expected to manage their portfolios to guard simultaneously against the risks of inflation and market collapse) and opened them up to exploitation by our financial sector (which sells them products designed to maximize bank fees rather than retirement security). Our mortgage system was our Achilles’ heel, and we have not really fixed it. With such a large fraction of Americans living in cities, we have to have urban housing policies that ensure affordable housing for all.

It is a long agenda—but a doable one. When skeptics say it is nice but not affordable, I reply: We cannot afford to not do these things. We are already paying a high price for inequality, but it is just a down payment on what we will have to pay if we do not do something—and quickly. It is not just our economy that is at stake; we are risking our democracy.

As more of our citizens come to understand why the fruits of economic progress have been so unequally shared, there is a real danger that they will become open to a demagogue blaming the country’s problems on others and making false promises of rectifying “a rigged system.” We are already experiencing a foretaste of what might happen. It could get much worse.

Joseph E. Stiglitz is a University Professor at Columbia University and Chief Economist at the Roosevelt Institute. He received the Nobel prize in economics in 2001. Stiglitz chaired the Council of Economic Advisers from 1995–1997, during the Clinton administration, and served as the chief economist and senior vice president of the World Bank from 1997–2000. He chaired the United Nations commission on reforms of the international financial system in 2008–2009. His latest authored book is Globalization and Its Discontents Revisited (2017).