Black homeownership is often caught up in the institutional failures of the past and the continued transgressions today.

For Mel Ligon and his wife, remnants of the 2008 housing crisis kept them from realizing major savings from refinancing their Chicago home during the pandemic refi boom.

They had a deferred principal placed on their home during the Great Recession when they used a government program to refinance after their household income dropped by half. About a decade later, that prevented them from benefiting from the historically low mortgage rates.

“Even when homes started to recover, we have this $88,000 deferred principal, which in essence would be our equity in the future that we wouldn’t have access to until 2050,” Ligon, an independent real estate broker, said.

Unfortunately, their story isn’t unique and instead illustrates how Black homeownership is often caught up in the institutional failures of the past and the continued transgressions today such as appraisal bias, mortgage discrimination, and even redlining.

And as housing affordability quickly erodes with rapidly higher mortgage rates and another potential recession looming on the horizon, the pursuit of the American Dream again becomes harder for many Blacks to achieve and, with it, the chance to build intergenerational wealth.

“The damaging impacts of high interest rates and inflation are already clear and disproportionately harmful to Black households,” according to the 2022 State of Housing in Black America (SHIBA) report. “Because higher mortgage interest rates decrease home purchase affordability, Blacks, relative to Whites, will be further disadvantaged in their homeownership search.”

Scars of the Great Recession linger

While the homeownership obstacles Blacks face trace back to the founding of the country, the largest recent setback was the Great Recession.

Black homeownership was 48% before it was decimated by the 2008 foreclosure crisis characterized by irresponsible — and in some cases, predatory — lending that disproportionately affected communities of color.

“In the lead up to the Great Recession, white families with annual incomes of less than $30,000 were less likely, on average, to get subprime mortgages compared with Black families with incomes of more than $200,000,” according to a report by the Aspen Institute’s Financial Security Program (Aspen FSP).

In the years following the foreclosure crisis, Black homeownership fell and eventually hit a 50-year low in 2019 at 40.6% — lower than the rate in 1968 — and hasn’t returned to pre-Great Recession levels. At the same time, the white homeownership rate has exceeded pre-recession levels, according to the National Association of Real Estate Brokers (NAREB).

“It was 10 years before Black neighborhoods really started to see the turn,” Ligon said. “Our neighborhoods take a long time to recover.”

Then the pandemic hit, bringing its own disproportionate economic pain and job loss to the Black community.

Black homeowner (Photo: Getty Creative)

That kept many from taking advantage of historically low rates in the first year of the pandemic. For instance, Black homeowners received only 3.7% of the $5.3 billion in savings from pandemic refinances through October 2020, according to a Federal Reserve Bank of Boston study.

Black buyers similarly faced obstacles during the pandemic.

“Although mortgage rates reached all-time lows in 2021, not everybody was able to benefit from these low rates. During 2019 and 2021, the white homeownership rate rose by nearly 3 percentage points, while the homeownership rate for Black Americans rose by 2 percentage points,” Nadia Evangelou, senior economist and director of forecasting at the National Association of Realtors (NAR), said in a statement.

“With 7% mortgage rates, only 15% of Black households can currently afford to buy the typical home compared to 30% of white households. Thus, Black families may fall further behind in homeownership compared to their white counterparts.”

Already, many Black buyers have been pushed out of the market. Only 3% of homebuyers in 2022 were Black, according to data from the National Association of Realtors, half the share from 2021.

Continued bias today

Aside from the economic obstacles that disproportionately affected Black owners and buyers, the community also faces bias in many aspects of the home-buying or refinancing process.

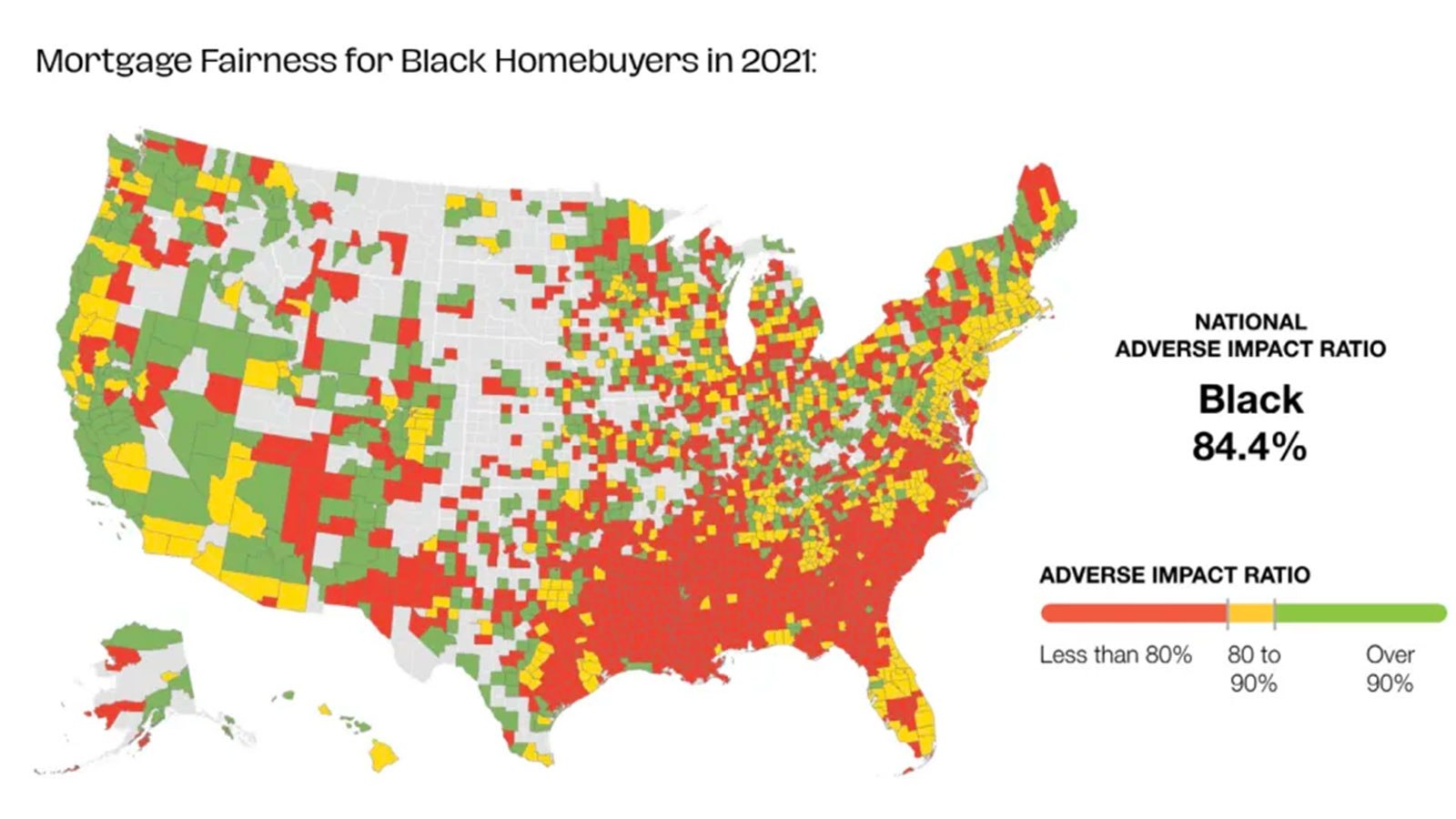

For instance, mortgage fairness for Black homebuyers has remained relatively static for the past 30 years, holding steady at 78.5% since 1990, according to the 2022 State of U.S. Mortgage Fairness (Fairness) report.

However, in 2021 mortgage fairness increased for Black mortgage applicants from 80.4% in 2020 to 84.4%, but the bump “reflects anomalous financial conditions during the COVID pandemic,” the report found.

And while the number of mortgage loan applications rose in 2021 for Black homebuyers, their loan denial rate of 15% far exceeded the 6% denial rate for white applicants, the SHIBA report found.

As interest rates reached 5% to 6%, mortgage fairness fell to almost 2008 housing crisis levels and got worse in areas with the highest concentration of Black homebuyers, the Fairness report found.

“Five states — Louisiana, Mississippi, South Carolina, Arkansas, and Alabama — yield persistently poor loan application outcomes no matter the macro environment…even in boom times,” the report found.

2022 State of U.S. Mortgage Fairness (Fairness) report

Even well-qualified minority homebuyers suffer discrimination, according to a 2012 HUD study.

Take, for example, the experience of former NFL player and actor, Devale Ellis and his wife Khadeen Ellis. The couple began looking for a luxury home in Georgia in 2020. Even with pre-approval from the bank, they encountered problems during underwriting.

“We originally wanted to put down 10%, but they said we had to put down 20%,” Devale Ellis said. “We agreed to put down 20% and they said we needed more than 20% after checking my credit score. My credit score is in the mid-700s!”

Hiring a CPA came in handy when the underwriters required three months of W-2s, even though Devale isn’t an employee and files a K-1 as an entertainer and business owner.

“It kills me that you work so hard to do everything the right way, only for people to find reasons not to allow you to have your dream. What if we weren’t in the position financially to pay more than 25% for a down payment?” Devale Ellis asked. “I know the vast majority of people in America live close to or below the poverty line, but it makes you realize how difficult it is for people who look like Khadeen and I to get property. It’s completely unfair because property is the way you build legacies.”

Instead of making it harder to qualify, some banks have simply stopped offering mortgage services to communities of color, known as modern day redlining.

Since 2021, the Department of Justice’s Combating Redlining Initiative announced four redlining cases and settlements against Lakeland Bank, Trident Bank, Trustmark National Bank, and Cadence Bank that adversely impacted Black and Hispanic homebuyers.

“Ending redlining is a critical step in our work to close the widening gaps in wealth between communities of color and others,” Assistant Attorney General Kristen Clarke of the Justice Department’s Civil Rights Division said in a press release. “[These] settlements demonstrate our firm commitment to combating modern day redlining and holding banks and other lenders accountable when they deny people of color equal access to lending opportunities.”

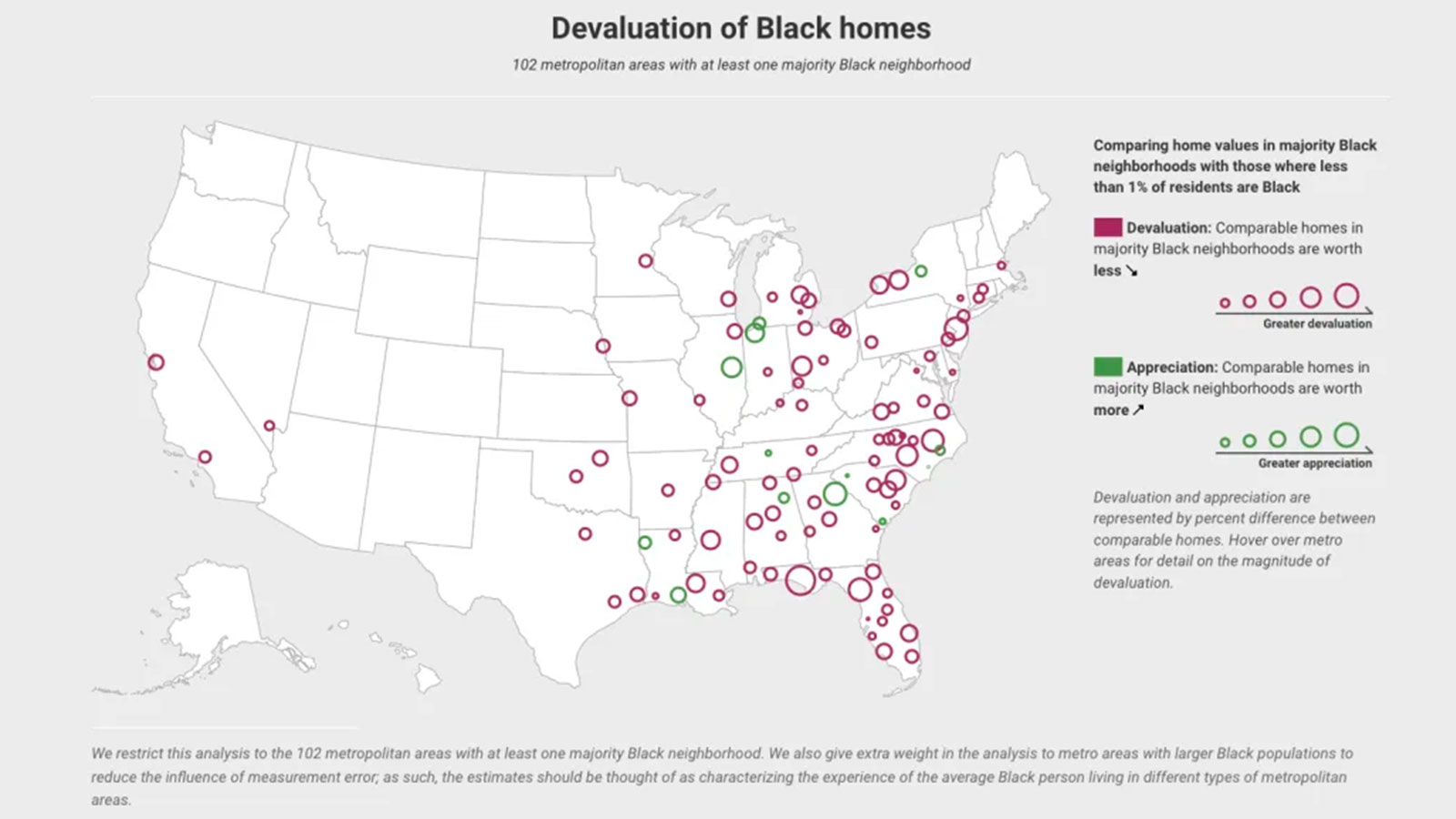

Appraisal bias devalues homes for Black homeowners

Black homebuyers and homeowners also face challenges during the home appraisal process.

For instance, Tenisha Tate-Austin and Paul Austin filed a lawsuit against the appraiser and the company that hired the appraiser for undervaluing their Marin County home in northern California by nearly $500,000, Caroline Peattie, executive director of Fair Housing Advocates of Northern California which represents the homeowners, told Yahoo Money.

A recent study by Freddie Mac found that “minority applicants are more likely to receive an appraisal value lower than the contract price.” Similarly, a 2022 Brookings Institute study found homes in neighborhoods that are 50% Black are valued 23% less compared with homes in other neighborhoods of similar quality and amenities.

The “cost of devaluation is approximately $162 billion” in cumulative losses for Black homeowners, the study concluded.

“It’s hard to not be discouraged in real estate as a Black realtor and for Black homebuyers and homeowners,” Kenyon Hunter, associate real estate broker at Evolution Ave Group RE, told Yahoo Money. “I had a white realtor call me after viewing my client’s home, a Black doctor. The realtor suggested that I have my client get rid of cultural elements — like a Doc McStuffins doll and African artwork — so that it would sell. I’ve noticed that if an appraiser recognizes a Black family lives there, the value goes down.”

2022 Brookings Institute study

Eroding affordability, delaying wealth

As mortgage rates increase, homeowners no longer have a chance to refinance and potential buyers find it more unaffordable to buy a home. Add in the discrimination they face in the mortgage and appraisal industries plus having high student debt balances and horizon for meaningfully increasing Black homeownership appears further away.

“A home purchase is the first tangible step in building wealth and for clients that didn’t have the liquidity or capital to save for a larger down payment, it’s discouraging to be left behind,” Chelsea Ransom-Cooper, managing partner and financial planning director at Zenith Wealth Partners, told Yahoo Money.

What homeownership offers is the chance to build generational wealth.

Housing equity accounts for 16% of total U.S. household wealth, according to a report by the Federal Reserve Bank of New York. For Black Americans, it’s even more than that. Nearly two-thirds of Black wealth is in housing, according NBER’s Wealth of Two Nations: The U.S. Racial Wealth Gap working paper.

“Homeownership is how the middle class builds wealth in America, and unfortunately Black homeowners often miss out on their fair share due to undervaluation,” Daryl Fairweather, Redfin’s chief economist, told Yahoo Money. “This not only hurts today’s Black homeowners, it also makes it harder for Black families to build intergenerational wealth, which has ripple effects throughout the Black community when it comes to educational attainment and business formation.”

Ronda is a personal finance senior reporter for Yahoo Money and attorney with experience in law, insurance, education, and government. Follow her on Twitter @writesronda

Source: Yahoo! Money

Featured image: An ‘open house’ flag is displayed outside a single family home on September 22, 2022 in Los Angeles, California. The U.S. housing market is seeing a slow down in home sales due to the Federal Reserve raising mortgage interest rates to help fight inflation. (Photo by Allison Dinner/Getty Images)